Federal Budget Announcements – Higher CGT, Harder Decisions

The 2026-2027 Federal budget has proposed some of the most significant changes to capital gains tax (CGT) in decades.

While much of the public discussion has focused on housing affordability, these measures go far beyond residential property. If enacted, they will materially impact how future investment decisions are made across property, shares, business structures and family groups.

What’s Changing?

- From 1 July 2027, the 50% CGT discount will be removed. This will be replaced with cost base indexation (linked to CPI) for assets held for more than 12 months.

- A minimum effective tax of 30% will apply to capital gains from this date as well.

- The proposed changes will be applied to all CGT assets held by individuals, trusts, and partnerships. This is not just a change for residential property, but commercial property, listed & unlisted shares – any CGT asset is affected.

- Pre-CGT assets (those acquired before 20 September 1985) which were previously exempt, are also party of this proposed change.

- Although commercial property have been excluded from the changes to negative gearing, it has not been excluded from the CGT reforms.

Transitional Rules

The Government has proposed a number of concessional transitional arrangements, but this is where the rules become significantly more technical and complex.

-

Assets sold before 1 July 2027

If you acquire and dispose of an asset before 1 July 2027, regardless of when the asset was purchased, the current rules will continue to apply and the capital gain will be calculated using the 50% CGT discount.

-

Assets held at 1 July 2027

For assets held at the start of the new rules, gains will be effectively split into two components:

-

- Pre-1 July 2027 gains – eligible for the CGT discount up to this date

- Post-1 July 2027 gains – calculated using the indexed cost base from the value as at this date, and will be subject to the 30% minimum tax rate

Each asset will be treated as having a reset cost base at 1 July 2027, from which the indexation calculation is applied.

-

Valuing assets at 1 July 2027

Taxpayers will need to determine the value of their assets at the transition date. At this stage the ATO has outlined two methods – either a formal market valuation, or the use of an ATO approved formula.

For business owners and those holding illiquid or complex assets, this valuation will be key. The higher the cost base at 1 July 2027, the lower the impact of the change to the indexation method & 30% minimum tax rate.

Business Owners

Business owners are particularly exposed under these changes. With shares often held at a nominal cost base, and indexation being the only uplift mechanism for businesses established post-1 July 2027, a future sale could see tax applied to almost the entire value created in the business.

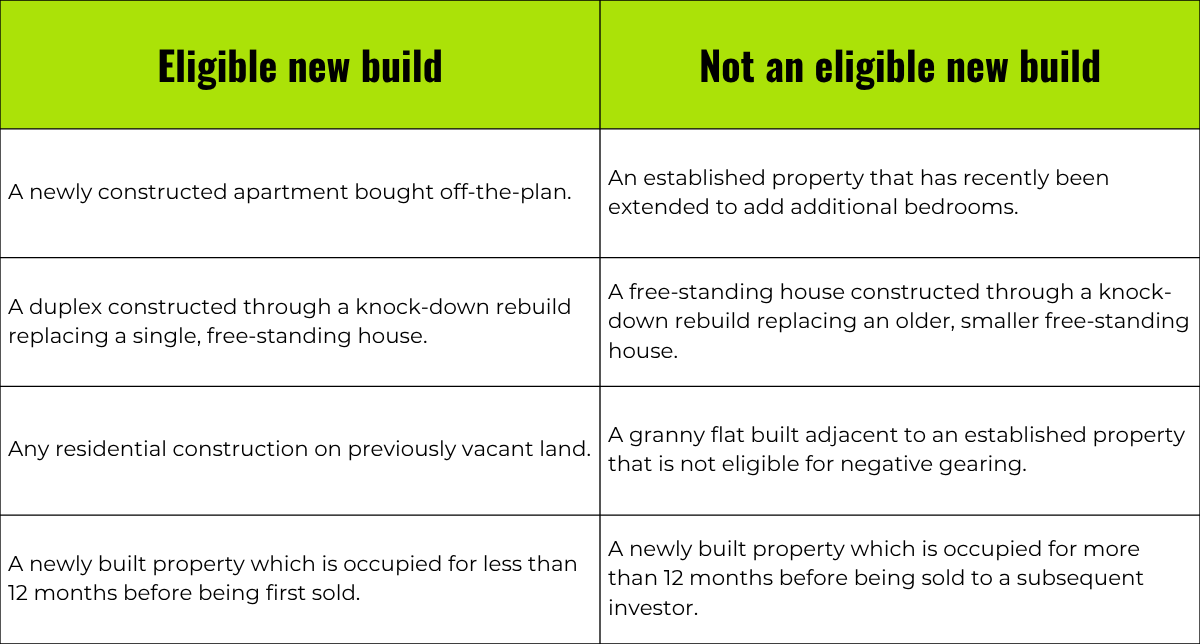

New Build Concession

The only asset type to be exempt from this new regime are eligible new residential builds. Investors in qualifying new builds will have the option to choose between the existing CGT discount, or the indexation & 30% minimum tax method.

Eligibility for what is a “new build” is tightly defined. The below table from the Budget papers outlines what is and isn’t eligible:

Source: Budget 2026-27 | Negative Gearing and Capital Gains Tax Reform papers.

What should you be doing now?

If the legislation is passed, you will want to consider the following, well before 1 July 2027:

- Review your current portfolio of assets and determine current exposure to the new rules

- Review your investment strategy

- Revisit your current structure to ensure it remains appropriate

- Scenario modelling to compare outcomes under current vs proposed rules, and timing considerations

- Planning for valuations, especially for businesses, private investments and property portfolios, that will be required for 1 July 2027.

While the Governments policy intent is framed around fairness and housing outcomes, the practical reality is that these changes introduce significantly more complexity and potentially higher tax consequences for investors.